Got a problem with Argentina being made to pay holdouts alongside its restructured bondholders?

Reckon it might happen to your sovereign (even if Argentina is apparently a “uniquely recalcitrant” debtor) and screw up its next debt restructuring?

Deal with it, says the Second Circuit of the United States Court of Appeals:

We can see that direct warning to redraft pari passu clauses being taken.

That’s the court dispatching all the wider fears about the pari passu saga and sovereign debt restructuring on Friday — even as it finally declared that it won’t accept Argentina’s suggested alternative for paying the holdouts. (Hardly a surprise — Argentina’s plan was a debacle.)

Some quick takes as we read the opinion on Friday…

First and foremost, ratable payment is go:

As the district court concluded, the amount currently owed to plaintiffs by Argentina as a result of its persistent defaults is the accelerated principal plus interest. We believe that it is equitable for one creditor to receive what it bargained for, and is therefore entitled to, even if other creditors, when receiving what they bargained for, do not receive the same thing.The reason is obvious: the first creditor is differently situated from other creditors in terms of what is currently due to it under its contract…

Right now, though, the Second Circuit’s ferocity is neutered because at the same time it’s also stayed the order to pay holdouts, while the Supreme Court decides whether to accept Argentina’s petition to review the case’s impact on sovereign immunity. Since the earliest the Supreme Court can do that is September, Argentina’s restructured payments before then might be OK, which is why we expect Argentine bonds would rally now.

Then again, that’s not such a long time, and the Second Circuit’s given no quarter. Even the hint of dissent’s tinier than an actual dissent — it’s literally a footnote:

Judge Pooler disagrees with the majority decision to dismiss the appeals of EBG, Fintech, Euro Bondholders, and ICE Canyon. However, as the arguments of the dismissed appellants are treated as made by amici, and as the status of the non-appellants matters little to the outcome here, Judge Pooler has agreed to note her disagreement for the record in this footnote, rather than dissent…

Third parties

That hint of dissent is still interesting though, as the Second Circuit ended up giving practically no ground to any third parties (including Bank of New York and clearing-houses) involved in Argentina paying its restructured bondholders. They therefore face serious legal risk beyond the stay (or any Supreme Court dismissal). And the Second Circuit does it all in very punchy language:

This type of harm—harm threatened to third parties by a party subject to an injunction who avows not to obey it—does not make an otherwise lawful injunction “inequitable.” We are unwilling to permit Argentina’s threats to punish third parties to dictate the availability or terms of relief…

When it comes to the restructured holders, the court bluntly tells them that they should have read their own bond contracts — where Argentina apparently warned that holdout litigation might stop payments to them. It also says that “if Argentina decides to default on the Exchange Bonds… Exchange Bondholders would then be able to sue over that default“. (Emphasis ours.)

We sense that’s going to be cold comfort.

The court’s answer to third parties tied to the payments system itself is more technical in terms of the law (BNY’s interventions in this case in particular have been all about how civil procedure works) but no less sweeping:

BNY and Euro Bondholders argue that the district court erred by purporting to enjoin payment system participants over which it lacks personal jurisdiction. But the district court has issued injunctions against no one except Argentina. Every injunction issued by a district court automatically forbids others—who are not directly enjoined but who act “in active concert or participation” with an enjoined party—from assisting in a violation of the injunction…The amended injunctions simply provide notice to payment system participants that they could become liable… if they assist Argentina in violating the district court’s orders.

Effectively the likes of BNY are being told to go back to Judge Griesa for clarification on whether the holdouts can file suit against them, the next time Argentina tries to pay restructured holders without paying NML et al, and without the stay in place. It’s very hard to see BNY sticking around for long as the trustee for the restructured bonds in these circumstances.

Even Argentina’s foreign-law bondholders — who have been up in arms, and ready to go to Belgian courts to effect a Mexican standoff with US judges over their right to be paid — get short shrift:

If ICE Canyon and the Euro Bondholders are correct in stating that the payment process for their securities takes place entirely outside the United States, then the district court misstated that, with the possible exception of Argentina’s initial transfer of funds to BNY, the Exchange Bond payment “process, without question takes place in the United States.”… But this possible misstatement is of no moment because, again, the amended injunctions enjoin no one but Argentina……We have never been presented with the question whether U.S. sanctions legally apply to non-U.S. persons or institutions, and we do not answer that question today. We merely note that both foreign and domestic financial institutions are already required to police their own transactions in order to avoid violations of potentially applicable United States laws and regulations…

Pari passu and the public interest

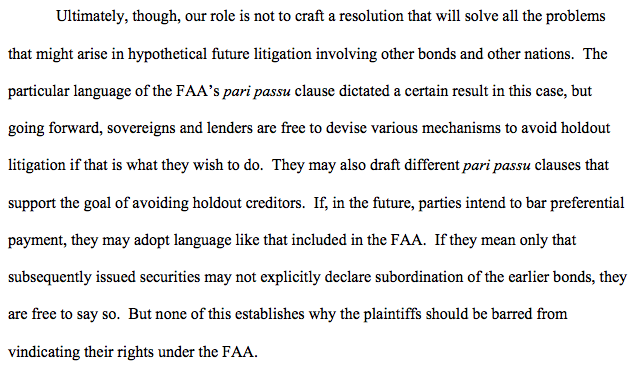

Ultimately the real fireworks are at the end though: it’s this question of precedent for sovereign debt restructuring, and whether ratable payment built on pari passu will now convince more bondholders to become holdouts at the margin. It’s slightly curious in that this stuff was never going to decisively sway the case one direction or the other.

Still, the Second Circuit comes over very defensive here:

Our decision here does not control the interpretation of all pari passu clauses or the obligations of other sovereign debtors under pari passu clauses in other debt instruments. As we explicitly stated in our last opinion, we have not held that a sovereign debtor breaches its pari passu clause every time it pays one creditor and not another, or even every time it enacts a law disparately affecting a creditor’s rights… We simply affirm the district court’s conclusion that Argentina’s extraordinary behavior was a violation of the particular pari passu clause found in the FAA.

Really? Actually we think that explicit statement is not all it appears. And that’s because the NML v Argentina legacy for the uses and abuses of pari passu has already begun to be litigated for other sovereigns.

After all, here’s a US district court judge holding forth in Ex-Im Bank v Grenada this week (basically to confirm that more work is needed in that case to see if Grenada’s been as “recalcitrant” a debtor as Argentina):

The fact is that in NML, the Second Circuit specifically left open the question of whether “a breach would occur with any non-payment that is coupled with payment on other debt . . . . [or] whether ‘legislative enactment’ alone could result in a breach” and chose to “simply affirm the district court’s conclusion that Argentina’s course of conduct here did.”

The Second Circuit didn’t explicitly state that pari passu breaches can be any time one creditor gets money and another doesn’t, that’s true — but they didn’t explicitlyrule it out either. They’ve now passed up another opportunity to clear it up. That could be a huge fissure in pari passu litigation going forward.

Lastly, the court once again points to collective action clauses as anti-holdout devices which will prevent another Argentina. Even if holdouts get enough votes to block a CAC, “a restructuring failure on one series would still allow restructuring of the remainder of a sovereign’s debt,” says the court. So is losing one series an acceptable level of violence for a restructuring? It’s an interesting question — Greece famously won massive, 90 per cent plus acceptance of its PSI last year through (local-law) CACs. But you still see huge anger over having to pay billions of euros in foreign-law bonds which failed to CAC.

Some are probably going to want to see that abortive IMF amicus brief eventually surface at the Supreme Court on these issues after all…