hier gehts Grenada pari passu mässig an den Kragen....

hier gehts Grenada pari passu mässig an den Kragen....

PLAINTIFF(S) ADDRESS(ES) AND COUNTY(IES)

The Export-Import Bank of the Republic of China

3 Nanhai Road, 8th Floor

Taipei (100) Taiwan

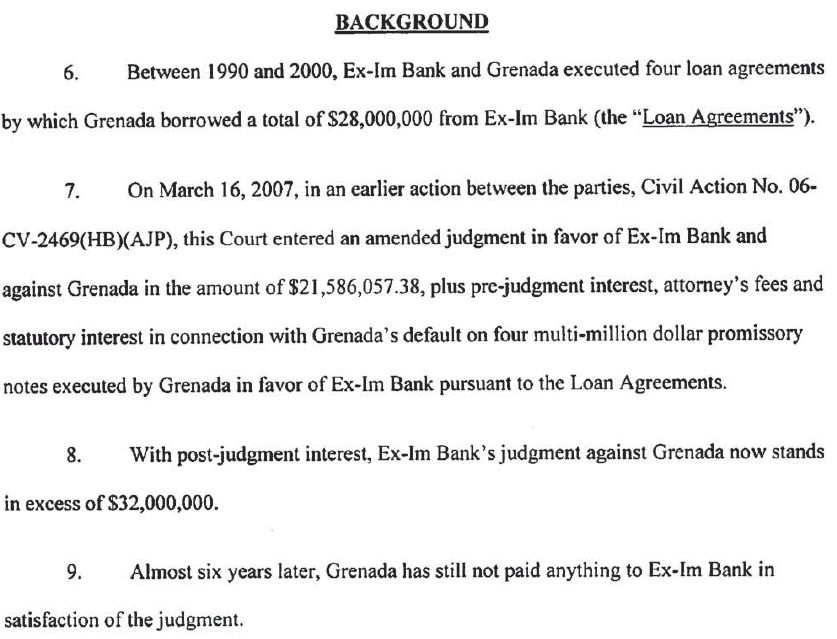

Republic of China

DEFENDANT(S) ADDRESS(ES) AND COUNTY(IES)

Grenada

Ministry of Finance

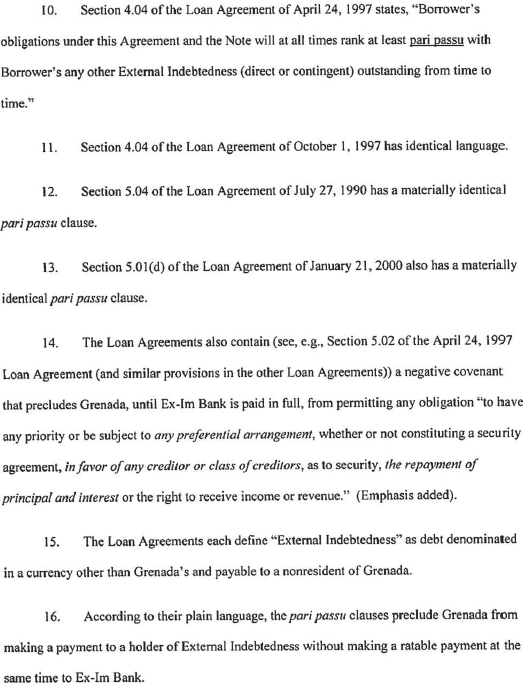

Financial Complex

Carenage, St. George's, Grenada

Paul E. Summit

Andrew T. Solomon

SULLIVAN & WORCESTER LLP

1633 Broadway

New York, NY 10019

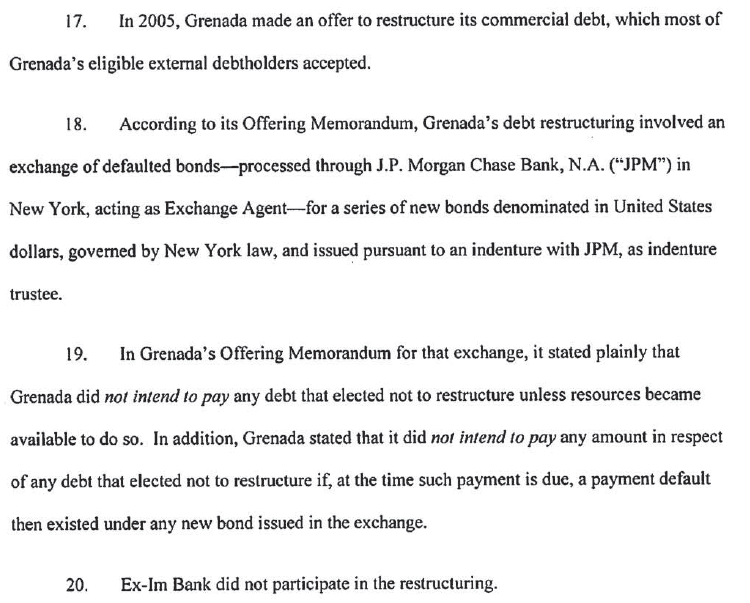

(212)660-3000

Attorneys fo r Plaintiff/Judgment Creditor

UNITED STATES DISTRICT COURT

SOUTHERN DISTRICT OF NEW YORK

THE EXPORT-IMPORT BANK OF

THE REPUBLIC OF CHINA,

-X

Plaintiff/Judgment Creditor,

-against-

GRENADA,

Defendant/Judgment Debtor.

-X

i l

Civil Action No:

COMPLAINT

Ca í

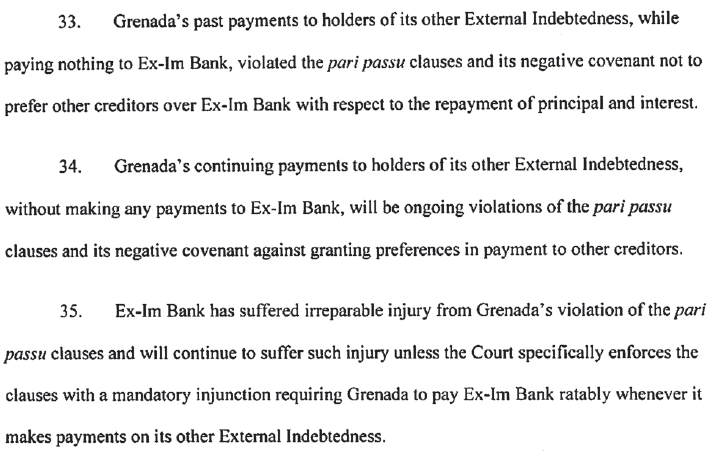

•'C

I

Plaintiff The Export-Import Bank of the Republic of China (“Ex-Im Bank”), by its-*7"

—

attorneys, Sullivan & Worcester LLP, complains of the defendant Grenada as follows^

• ••

JURISDICTION AND VENUE o '

I. This court has jurisdiction over the subject matter of this action pursuant to 28

U.S.C.§ 1330.

2. Venue properly exists in this district pursuant to 28 U.S.C. § 1391(f), based upon

the residence and status o f the parties, the events and omissions giving rise to the claims, and the

agreement which provides the basis for this action.

3. In addition, Grenada irrevocably consented to the non-exclusive jurisdiction of

any State or Federal Court in New York, New York, to waive any objection to that venue on any

ground, and to accept service o f process by registered or certified mail to the notice address

provided in the agreements at issue.

THE PARTIES

4. Ex-Im Bank is a banking institution organized and existing under the laws of the

Republic of China, with its principal place o f business in Taipei, the Republic of China. The

business of Ex-Im Bank includes the lending of money internationally.

5. Grenada is a foreign state as defined in 28 U.S.C. § 1603(a).

BACKGROUND

6. Between 1990 and 2000, Ex-Im Bank and Grenada executed four loan agreements

by which Grenada borrowed a total o f $28,000,000 from Ex-Im Bank (the “Loan Agreements”).

7. On March 16, 2007, in an earlier action between the parties, Civil Action No. 06-

CV-2469(HB)(AJP), this Court entered an amended judgment in favor o f Ex-Im Bank and

against Grenada in the amount o f $21,586,057.38, plus pre-judgment interest, attorney’s fees and

statutory interest in connection with Grenada’s default on four multi-million dollar promissory

notes executed by Grenada in favor o f Ex-Im Bank pursuant to the Loan Agreements.

8. With post-judgment interest, Ex-Im Bank’s judgment against Grenada now stands

in excess of $32,000,000.

9. Almost six years later, Grenada has still not paid anything to Ex-Im Bank in

satisfaction o f the judgment.

10. Section 4.04 o f the Loan Agreement o f April 24, 1997 states, “Borrower’s

obligations under this Agreement and the Note will at all times rank at least pari passu with

Borrower’s any other External Indebtedness (direct or contingent) outstanding from time to

time.”

11. Section 4.04 o f the Loan Agreement o f October 1, 1997 has identical language.

12. Section 5.04 o f the Loan Agreement of July 27, 1990 has a materially identical

pari passu clause.

13. Section 5.01(d) of the Loan Agreement of January 21,2000 also has a materially

identical pari passu clause.

14. The Loan Agreements also contain (see, e.g., Section 5.02 o f the April 24,1997

Loan Agreement (and similar provisions in the other Loan Agreements)) a negative covenant

that precludes Grenada, until Ex-Im Bank is paid in full, from permitting any obligation “to have

any priority or be subject to any preferential arrangement, whether or not constituting a security

agreement, in favor o f any creditor or class o f creditors, as to security, the repayment o f

principal and interest or the right to receive income or revenue.” (Emphasis added).

15. The Loan Agreements each define “External Indebtedness” as debt denominated

in a currency other than Grenada’s and payable to a nonresident of Grenada.

16. According to their plain language, the pari passu clauses preclude Grenada from

making a payment to a holder of External Indebtedness without making a ratable payment at the

same time to Ex-Im Bank.

3

17. In 2005, Grenada made an offer to restructure its commercial debt, which most of

Grenada’s eligible external debtholders accepted.

18. According to its Offering Memorandum, Grenada’s debt restructuring involved an

exchange o f defaulted bonds—processed through J.P. Morgan Chase Bank, N.A. (“JPM”) in

New York, acting as Exchange Agent—for a series o f new bonds denominated in United States

dollars, governed by New York law, and issued pursuant to an indenture with JPM, as indenture

trustee.

19. In Grenada’s Offering Memorandum for that exchange, it stated plainly that

Grenada did not intend to pay any debt that elected not to restructure unless resources became

available to do so. In addition, Grenada stated that it did not intend to pay any amount in respect

of any debt that elected not to restructure if, at the time such payment is due, a payment default

then existed under any new bond issued in the exchange.

20. Ex-Im Bank did not participate in the restructuring.

21. Upon information and belief, Grenada also received debt relief from the Paris

Club in 2006, resulting in the rescheduling of its obligations to bilateral creditors including

Belgium, the United Kingdom, the United States, and France.

22. Upon information and belief, in connection with the 2005 and the Paris Club

restructurings, Grenada has been making substantial interest payments on its external debt for

years, to the tune of over $43,000,000 (approximately $8,242,000 in 2008, $11,429,000 in 2009,

$11,478,000 in 2010, and $12,443,000 in 2011).

4

23. As recently as October 15,2012, Grenada paid a full interest payment to the

holders of a $193,000,000 bond arising from the 2005 debt restructuring.

24. At least a portion of these payments are being made through Grenada’s paying

agent, the Bank of New York Mellon (global headquarters at One Wall Street, New York, NY).

25. In a prospectus for the refinancing of Grenada treasury bills in November 2012,

Grenada (1) claimed that it “has witnessed a remarkable recovery” since Hurricanes Ivan and

Emily in 2004 and 2005; (2) highlighted its 2005 commercial debt restructuring, the debt relief it

received from the Paris Club, its years-long participation in IMF economic reform programs, and

its establishment of a Debt Management Unit within its Ministry of Finance; and (3) stated that it

“has an exemplary record” of repaying all issues of treasury bills since Grenada’s entry into that

market.

26. In the earlier action between the parties, Grenada has made many efforts to evade

responsibility for its debts to Ex-Im Bank.

27. Ex-Im Bank has been damaged as a result of Grenada’s violations o f the pari

passu clauses and will continue to be damaged by the ongoing violations.

CLAIM FOR SPECIFIC ENFORCEMENT OF THE PARI PASSU CLAUSES AND THE

NEGATIVE COVENANT FOR INJUNCTIVE RELIEF

28. Ex-Im Bank repeats and re-alleges the allegations set forth in paragraphs 1

through 25 herein.

29. Pursuant to the pari passu clauses of the Loan Agreements, Grenada guaranteed

that, “Borrower’s obligations under this Agreement and the Note will at all times rank at least

5

pari passu with Borrower’s any other External Indebtedness (direct or contingent) outstanding

from time to time.”

30. Grenada, therefore, may not make any payment of its External Indebtedness

without also making a ratable payment at the same time to Ex-Im Bank.

31. Pursuant to the negative covenant, described in paragraph 14 above, Grenada

promised not to enter into any “preferential arrangement” with any “class o f creditors” as to “the

repayment of principal and interest.”

32. Grenada, therefore, may not enter into any agreement other creditors under which

it prefers those creditors as to the payment of principal and interest above its obligation to pay

Ex-Im Bank.

33. Grenada’s past payments to holders of its other External Indebtedness, while

paying nothing to Ex-Im Bank, violated the pari passu clauses and its negative covenant not to

prefer other creditors over Ex-Im Bank with respect to the repayment o f principal and interest.

34. Grenada’s continuing payments to holders of its other External Indebtedness,

without making any payments to Ex-Im Bank, will be ongoing violations o f the pari passu

clauses and its negative covenant against granting preferences in payment to other creditors.

35. Ex-Im Bank has suffered irreparable injury from Grenada’s violation of the pari

passu clauses and will continue to suffer such injury unless the Court specifically enforces the

clauses with a mandatory injunction requiring Grenada to pay Ex-Im Bank ratably whenever it

makes payments on its other External Indebtedness.

6

36. Remedies available at law are inadequate to compensate for such injury.

37. Ex-Im Bank has performed its part of the Loan Agreements with Grenada.

38. The balance of equities tips overwhelmingly toward the issuance o f an injunction.

39. The public interest would not be harmed by the issuance of a permanent

injunction.

WHEREFORE, Ex-Im Bank demands judgment against Grenada (1) specifically

enforcing the pari passu clauses and the negative covenant against granting preferential payment

arrangements to other creditors, and (2) awarding Ex-Im Bank its costs, prejudgment interest,

attorneys’ fees and such other and further relief as the Court shall deem just and proper.

Dated: New York, New York SULLIVAN & WORCESTER LLP

March 4,2013

Paul E. Summit

Andrew T. Solomon

1633 Broadway

New York, NY 10019

T. 212.660.3000

F. 212.660.3001

Attorneys for Plaintiff/Judgment Creditor The Export-

Import Bank o f the Republic o f China

7