Grenada Is Not Argentina

Some in the financial markets have had mixed reactions to the U.S. Court of Appeals for the Second Circuit’s NML Capital, Ltd. v. Republic of Argentina decision, which required Argentina to treat all of its bondholders equally. On the one hand, they are happy that the decision prevents solvent debtors like Argentina from making take-it-or-leave-it demands to bondholders and refusing all payments to those who don’t knuckle under. On the other hand, some Cassandras warn that the decision’s protections for the rights of holdout bondholders will prevent nations facing financial crises from undertaking an orderly restructuring of their debts.

A decision handed down yesterday by a federal district court in New York, Export-Import Bank of China v. Grenada, should put to rest many of those concerns. The decision, issued in connection with claims against the island nation of Grenada, makes clear that the NML decision is limited to Argentina’s unique status as a deadbeat debtor willing to thumb its nose at its legitimate creditors. Mere nonpayment by sovereign nations acting in good faith, the court explained, will not trigger the sort of injunctive relief for bondholders that the Second Circuit upheld inNML.

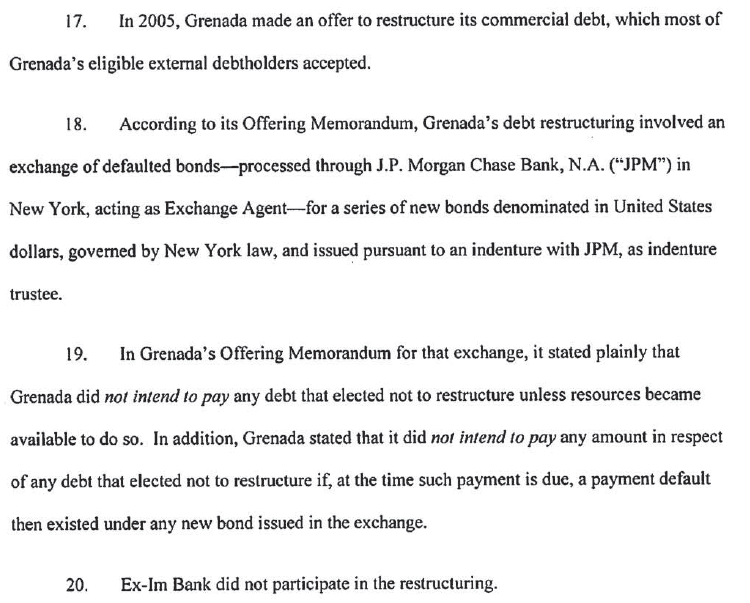

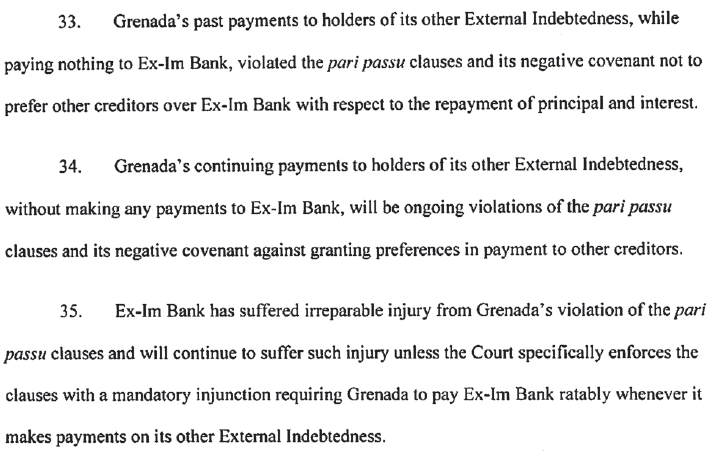

Earlier this year, the Export-Import Bank of the Republic of China (“Ex-Im Bank”) filed suit against Grenada, seeking to enforce a pari passu clause in its loan agreement with the nation. In 2005, following financial setbacks caused by Hurricanes Ivan and Emily, Grenada sought to restructure its foreign debt. The Ex-Im Bank did not participate in the restructuring and instead obtained a court judgment on its debt. Since then, Grenada has made some interest payments on its restructured debt but has paid nothing to Ex-Im Bank. Apparently hoping to piggy-back on the NML decision, Ex-Im sought an injunction against any further interest payments to holders of Grenada’s restructured debt unless payments were also made to Ex-Im Bank.

The district court yesterday denied Ex-IM’s motion for judgment on the pleadings, explaining that the NML injunction had been based on a unique set of circumstances. Argentina did not merely fail to make payments to some bondholders while making interest payments to others; it also took numerous executive and legislative actions designed to ensure that, in direct violation of “equal treatment” promises it made as part of its pari passu clause, the debt held by disfavored bondholders would be effectively subordinated to debt held by other bondholders. Indeed, Argentina went so far as to adopt a “Lock Law” that prohibited all payments to bondholders who did not accept its take-it-or-leave-it restructuring offer, and to declare those bonds unenforceable in Argentina’s own courts.

The district court held that Ex-Im did not allege any similar conduct by Grenada. While noting that Grenada is alleged to have made occasional payments to other creditors since it stopped making payments to Ex-Im in 2008, the court held that Grenada’s payment history did not demonstrate anything approaching the sort of discriminatory treatment that gave rise to the NML injunction against Argentina. Indeed, the court noted that earlier this year Grenada announced that it did not have the resources to make even the interest payments on its bonds, and that it would seek once again to restructure its debts.

The Ex-Im Bank will still have an opportunity, following completion of pre-trial discovery, to attempt to prove that Grenada has engaged in same sort of discriminatory conduct that led the Second Circuit to uphold injunctive relief against Argentina. But yesterday’s decision should put to rest concerns that pari passu litigation may “go viral.” The court said that, even assuming that Ex-Im Bank could show that the pari passu clause agreed to by Grenada is as fulsome as the one at issue in NML – a doubtful assumption, based on my reading of the documents — Ex-Im could not obtain injunctive relief in the absence of a showing, similar to the one made against Argentina, that Grenada took steps to effectively block all prospect of future payment on Ex-Im indebtedness.

The disparate circumstances facing Grenada and Argentina undoubtedly played a role in yesterday’s district court decision. Grenada is a poor nation which is in arrears on all its foreign debt. Grenada is treating Ex-Im Bank and all other creditors the same; it’s not paying any of them. Argentina’s economy, on the other hand, is recovering nicely, and the Second Circuit determined that Argentina has more than sufficient foreign reserves to pay all its debts to bondholders. Argentina is not paying holdout bondholders because it chooses not to; as the district court recognized, Grenada is not paying Ex-Im Bank because, at least in the near term, it can’t.

Finally, one needs to remember that the federal courts did not enter injunctive relief until after having to endure nearly a decade of Argentina’s flat-out refusals to honor its debt obligations. Argentina’s infamous Lock Law prohibited treasury officials from paying so much as a penny to bondholders who were unwilling to accept the nation’s take-it-or-leave-it proposal of a 70 percent haircut. The patient approach that federal courts adopted for so many years in response to Argentinian intransigence is a strong indication that they will enforce equitable-treatment obligations imposed by pari passu clauses only after they become convinced that a sovereign debtor has abandoned all pretense of fairness among its creditors. Yesterday’s decision is one more indication that the federal courts will not allow holdout creditors to disrupt reasonable bond-restructuring efforts.

— Rich Samp is chief counsel for litigation at the Washington Legal Foundation.

http://www.nationalreview.com/bench-memos/356463/grenada-not-argentina-rich-samp

A decision handed down yesterday by a federal district court in New York, Export-Import Bank of China v. Grenada, should put to rest many of those concerns. The decision, issued in connection with claims against the island nation of Grenada, makes clear that the NML decision is limited to Argentina’s unique status as a deadbeat debtor willing to thumb its nose at its legitimate creditors. Mere nonpayment by sovereign nations acting in good faith, the court explained, will not trigger the sort of injunctive relief for bondholders that the Second Circuit upheld inNML.

Earlier this year, the Export-Import Bank of the Republic of China (“Ex-Im Bank”) filed suit against Grenada, seeking to enforce a pari passu clause in its loan agreement with the nation. In 2005, following financial setbacks caused by Hurricanes Ivan and Emily, Grenada sought to restructure its foreign debt. The Ex-Im Bank did not participate in the restructuring and instead obtained a court judgment on its debt. Since then, Grenada has made some interest payments on its restructured debt but has paid nothing to Ex-Im Bank. Apparently hoping to piggy-back on the NML decision, Ex-Im sought an injunction against any further interest payments to holders of Grenada’s restructured debt unless payments were also made to Ex-Im Bank.

The district court yesterday denied Ex-IM’s motion for judgment on the pleadings, explaining that the NML injunction had been based on a unique set of circumstances. Argentina did not merely fail to make payments to some bondholders while making interest payments to others; it also took numerous executive and legislative actions designed to ensure that, in direct violation of “equal treatment” promises it made as part of its pari passu clause, the debt held by disfavored bondholders would be effectively subordinated to debt held by other bondholders. Indeed, Argentina went so far as to adopt a “Lock Law” that prohibited all payments to bondholders who did not accept its take-it-or-leave-it restructuring offer, and to declare those bonds unenforceable in Argentina’s own courts.

The district court held that Ex-Im did not allege any similar conduct by Grenada. While noting that Grenada is alleged to have made occasional payments to other creditors since it stopped making payments to Ex-Im in 2008, the court held that Grenada’s payment history did not demonstrate anything approaching the sort of discriminatory treatment that gave rise to the NML injunction against Argentina. Indeed, the court noted that earlier this year Grenada announced that it did not have the resources to make even the interest payments on its bonds, and that it would seek once again to restructure its debts.

The Ex-Im Bank will still have an opportunity, following completion of pre-trial discovery, to attempt to prove that Grenada has engaged in same sort of discriminatory conduct that led the Second Circuit to uphold injunctive relief against Argentina. But yesterday’s decision should put to rest concerns that pari passu litigation may “go viral.” The court said that, even assuming that Ex-Im Bank could show that the pari passu clause agreed to by Grenada is as fulsome as the one at issue in NML – a doubtful assumption, based on my reading of the documents — Ex-Im could not obtain injunctive relief in the absence of a showing, similar to the one made against Argentina, that Grenada took steps to effectively block all prospect of future payment on Ex-Im indebtedness.

The disparate circumstances facing Grenada and Argentina undoubtedly played a role in yesterday’s district court decision. Grenada is a poor nation which is in arrears on all its foreign debt. Grenada is treating Ex-Im Bank and all other creditors the same; it’s not paying any of them. Argentina’s economy, on the other hand, is recovering nicely, and the Second Circuit determined that Argentina has more than sufficient foreign reserves to pay all its debts to bondholders. Argentina is not paying holdout bondholders because it chooses not to; as the district court recognized, Grenada is not paying Ex-Im Bank because, at least in the near term, it can’t.

Finally, one needs to remember that the federal courts did not enter injunctive relief until after having to endure nearly a decade of Argentina’s flat-out refusals to honor its debt obligations. Argentina’s infamous Lock Law prohibited treasury officials from paying so much as a penny to bondholders who were unwilling to accept the nation’s take-it-or-leave-it proposal of a 70 percent haircut. The patient approach that federal courts adopted for so many years in response to Argentinian intransigence is a strong indication that they will enforce equitable-treatment obligations imposed by pari passu clauses only after they become convinced that a sovereign debtor has abandoned all pretense of fairness among its creditors. Yesterday’s decision is one more indication that the federal courts will not allow holdout creditors to disrupt reasonable bond-restructuring efforts.

— Rich Samp is chief counsel for litigation at the Washington Legal Foundation.

http://www.nationalreview.com/bench-memos/356463/grenada-not-argentina-rich-samp